25 Years of San Lorenzo Valley Real Estate Cycles

Boom, Bust, Fire & Recalibration

By MaryBeth McLaughlin, The MountainEar

If you’ve lived in the San Lorenzo Valley long enough, you know something important: Nothing here moves in straight lines. Not the roads. Not the creeks. And certainly not the real estate market.

For years, conversations have swung between optimism and concern — interest rates, insurance shifts, fire recovery, policy changes. But when we zoom out and look at twenty-five years of local data, the story looks less dramatic and more… cyclical. And like tree rings. Each year leaves a mark.

Homes: Shelter First, Investment Second

Homes in Boulder Creek, Brookdale, Ben Lomond, Felton, Zayante, and Lompico are still selling. From small creekside cabins to ridge-top estates, transactions continue across price points. But buyers are moving differently now. They’re slower in their decision making, more deliberate, and less emotional.

Well-priced homes in solid, livable condition are attracting attention. Properties with deferred maintenance, difficult access, or insurance challenges are taking longer — sometimes requiring strategic price adjustments. This is not a frozen market. It’s a selective one.

Insight: Homes move when life moves — jobs, families, school districts, financing. Even in uncertain cycles, people still need shelter.

Land: The “What Could This Become?” Question

Land is different. Unlike a home — where value is visible — land value hides underground. Sometimes literally. Two parcels can share the same asking price but have entirely different futures. In the mountains, buildability is shaped by:

- Zoning (Timber Production, Residential Agriculture, etc.)

- Road access and fire truck standards

- Septic feasibility

- Water availability

- Slope and geology

- Prior legal building rights

- Fire history and entitlement status

In recent years, construction costs have climbed. Labor, materials, insurance, permitting — all more expensive. When build costs rise, raw land doesn’t automatically become more valuable. Sometimes the opposite happens: feasibility tightens.

Insight: Today’s land buyers aren’t speculating. They’re calculating.

Then Came the Fire

August 2020 changed the landscape — physically and administratively. Nearly 1,000 properties were affected in the CZU Lightning Complex Fire. Rebuild timelines, entitlement uncertainty, and insurance shifts reshaped land turnover.

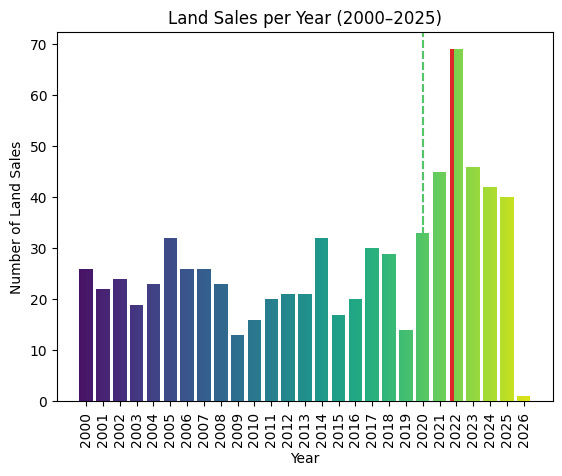

- Land sales in 2019: 14

- Land sales in 2020: 33

- Land sales in 2021: 45

- Land sales in 2022: 69

2022 stands out like a burn scar on a hillside — an unmistakable spike. Since then? Activity has tapered. It hasn’t collapsed; it has normalized. The increase in land sales in 2021 and especially 2022 was likely driven by a combination of factors rather than one single cause. Immediately after the August 2020 fire, many property owners were still assessing insurance coverage and feasibility. By 2021, several realities had set in:

- Some owners were uninsured or significantly underinsured and simply could not afford to rebuild.

- Construction costs escalated dramatically post-fire and during COVID, widening funding gaps.

- The emotional toll was real — some residents were traumatized and did not want to endure a multi-year rebuilding process.

At the same time, there were countervailing forces:

- COVID migration increased rural demand beginning in late 2020 and continuing into 2021.

- The County established the Recovery Permit Center to streamline rebuilds and reduce fees for original fire victims.

- Buyers from outside the area saw opportunity in cleared parcels with prior entitlements.

However, as debris-flow modeling and hazard mapping were formalized in late 2021 (Atkins study rollout), rebuilding in certain areas became more complex and, in some cases, more costly. That introduced additional uncertainty for some owners. Then on October 25, 2022, the Board of Supervisors adopted the new septic point-of-sale ordinance (effective July 1, 2023), requiring inspection and, if necessary, permitted repair prior to transfer. While that rule came after the 2022 peak, the broader regulatory environment was becoming more defined — and more rigorous.

So in summary, I would characterize the 2021–2022 land sales spike as the intersection of:

- Financial reality for fire victims (insurance gaps + construction inflation)

- Emotional fatigue and life resets

- Elevated rural demand during COVID

- Investors/speculators entering the market

- Increasing regulatory clarity around rebuilding and environmental constraints

It wasn’t simply “didn’t want to deal with the County,” though for some, regulatory complexity was certainly part of the calculus.

The Long View: 25 Years of “Land” Sales

If we compress 25 years of land sales into a short timeline, distinct cycles emerge:

2000–2002: Dot-com collapse

Silicon Valley equity wealth contracted sharply after March 2000. Stock-based compensation evaporated. Discretionary purchases — including rural land and second homes — slowed. Valley activity reflected that pullback.

2003–2007: Expansion + Rising Rural Appeal

Credit loosened. Home values climbed. Confidence returned. At the same time, larger rural parcels — particularly 10+ acre properties with water, privacy, and usable terrain — began attracting renewed interest. Agricultural flexibility, retreat potential, and increasing interest from Bay Area buyers looking for space outside urban cores contributed to steady demand.

2008–2010: Housing Crash, Local Resilience

Nationally, the financial crisis tightened lending and reduced liquidity. Yet certain rural parcels locally maintained interest. Agricultural flexibility, privacy, and alternative use potential supported demand even as broader housing markets contracted.

2011–2015: Peak Rural Acreage Demand

Large parcels with water access, sun exposure, and infrastructure capacity commanded strong pricing relative to long-term norms. Lifestyle buyers, agricultural users, and investors seeking retreat-style properties contributed to sustained activity. The early rise of short-term rental platforms also increased interest in rural investment properties.

2016–2018: Regulatory Transition and Market Shift

Statewide policy changes formalized agricultural licensing structures and introduced new compliance standards. While legitimacy increased, operating costs and regulatory oversight rose. At the same time, broader lifestyle migration into rural communities continued. Speculative land buying gradually cooled as economics and compliance tightened.

2019: 14 Land Sales

Regulatory adjustment, increased oversight, and market saturation reduced speculative momentum. The land market was already transitioning prior to the unrelated disruption of the 2020 fire.

2020–2022: Fire and Post-Fire Repositioning Surge

The CZU Lightning Complex Fire accelerated turnover. Rebuild rights, entitlement repositioning, insurance pressure, and pandemic-era migration created a measurable spike in activity — separate from earlier rural demand cycles.

2023–2025: Gradual Normalization

Higher interest rates, insurance shifts, and rising development costs reshaped underwriting assumptions. Pricing and volume returned closer to long-term historical ranges.

Over the years, our land market hasn’t been driven by just one thing. It moves with the broader economy — but also with changing lifestyles, new regulations, and opportunities unique to our mountains.

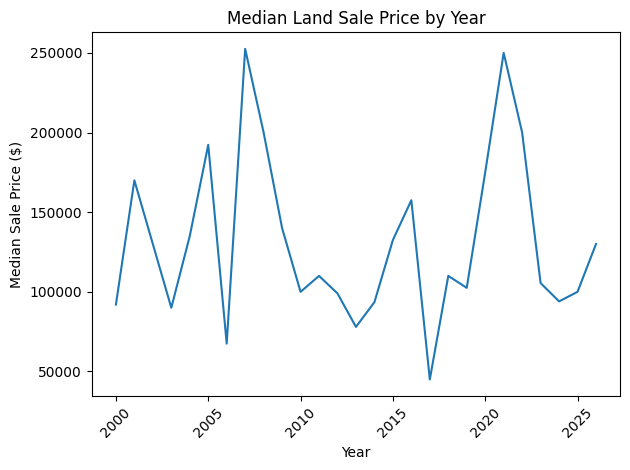

Price Tells a Second Story

Transaction volume peaked in 2022 and has gradually normalized. Median sale prices, however, tell an even clearer story. Land sale prices reached a recent high near $250,000 in 2021. By 2023–2025, median prices settled closer to $95,000–$105,000 — levels more consistent with the broader 20-year range. Again, a recalibration.

As development costs, insurance premiums, and entitlement complexity increased, buyers adjusted their risk assumptions. The market began discounting uncertainty more aggressively than acreage.

The Recent Pause

We’re already into March, and early activity this year remains measured. The past year felt slower — and the opening weeks of this year suggest a conservative pace unless interest rates shift meaningfully.

- Borrowing costs have reshaped affordability.

- Construction expenses remain elevated.

- Insurance coverage is available — often through the California FAIR Plan — but premiums are higher and coverage structures have changed.

Buyers are not absent. They are deliberate. They are running numbers carefully, evaluating total carrying costs, and underwriting more conservatively before writing offers. For existing homes, higher construction costs can help support replacement value. For vacant land, rising development expenses compress feasibility and elevate the importance of due diligence.

CZU Rebuild Clock

For parcels that previously held legal residences, rebuild windows are not indefinite. Sub-acre properties impacted by the 2020 fire must apply within 10 years to preserve rebuild rights. Transfers of ownership can introduce additional review standards. For some landowners, this is simply administrative housekeeping. For others, it may determine long-term value. Why? A sub-acre lot in the CZU burn zone that retains residential rebuild rights has real estate value. The same lot without those rights — because the window lapsed or a transfer introduced complications — could be worth a fraction of that, essentially just raw land with limited use.

What About Homes?

This issue focused primarily on land — because land and homes do not respond to cycles in the same way.

In next month’s column, we’ll look more closely at twenty-five years of Valley home sales — including pricing patterns, days on market, and how residential trends compare to the land cycles outlined here.

Final Thoughts, For Now

The San Lorenzo Valley market is not defined by headlines. It is defined by terrain, regulation, infrastructure, and feasibility. Homes that align with condition, price, and insurability are selling. Land that aligns with entitlement and buildability is moving.

MaryBeth McLaughlin

MaryBeth McLaughlinis a local Realtor specializing in mountain and rural properties throughout the Santa Cruz Mountains. She brings humor, heart,and hard data to every transaction — and now to her new monthly column.